New year, new resolutions.

Some people plan new year resolutions yearly. I wonder how many do they actually achieve. People think that in a year they can achieve huge lofty goals - earn a million dollars, buy a new property, find a new job etc.

Actually. What really matters is not the goal setting. But figuring out what is important to oneself. For example - in the pursuit of earning your first million, what is the purpose of that?

1. So that you achieve financial independence

2. So that you can buy that dream home

3. So that you can travel to exotic countries to experience their culture

Truly, time is the most precious resource. Recently I was watching Bill and Melinda gates on Jimmy Fallon show. It was fascinating to see how the world's richest man devoted so much time to making the world a better place - solving unnecessary Malaria deaths in third world countries. Improving standards of living, changing the world.

Now think of it...he could have continued in Microsoft and dominated the world, he could have made Microsoft the Google/Facebook/Apple of the world if they just kept pushing boundaries but Gates choose to retire and devote his life to more meaningful tasks.

Fascinating.

Now I do long term goals - my goals have turn lofty, some friends tell me its a stretch but sometimes we need to all try.

1. To grow my personal net worth by 20% yearly.

(The magic of compounding would allow for returns to reach 3800% within 20 years - which is my targeted retirement age at 50 years old.)

2. To move the direction of medical society in the right direction of improving how things work

3. To set up a foundation to help treat cancer patients

Saturday, December 31, 2016

Sunday, November 27, 2016

The philosophy of doing what you love and loving what you do

Recently, I celebrated my 27th birthday. It was a muted celebration. 2016 was not an easy year for me in terms of family, relationship, career and belief. Those closer to me would know that the passing storms make life really really 'suck'.

Everything faced a shadow of doubt, the echoes of failure, the difficulty of life, the lack of control, the pain of loss, the fear of the unknown, the difficulty of unpredictability - I faced them all.

The song of silence - by Simon & Garfunkel. A poignant soft song that echoed the sadness and grief in my heart.

I stared at the abyss of difficulty. I looked upward for answers but I found none. I look sideways to men, yet I found no comfort in those who could not empathize. I found myself increasingly frustrated by human's inability to connect.

Even though life is uncertain, I decidedly know that I must continue my journey. Life is a long stretch, its not easy, its going to hit you like a brick, a tsunami. You will face waves after wave of human disappointments, relationship problems, career issues - yet you can come out stronger after it because you believe that there is something important in life that you still must fulfill.

Life is not just about good results

Nor is it about accumulating greater wealth

Nor is it about gaining power

Nor is it about having all the things you ever wanted

No

It is about finding out your purpose

It is about living a life of purpose

It is about finding what you love

Which really led me to reflect. What would bring me happiness?

I begin to ponder what brought me fulfillment and meaning.

Ray Dalio once said - you can do anything you want, but you cannot do everything you want.

What an important statement.

As 2016 drew to a close, I thought long and hard about what mattered. At the end of life, what really matters?

Perhaps it really boils down to the following 3 questions:

1. Did I find and pursue my calling?

2. Am I a person who kept his promises?

3. Have I left a legacy?

For there is much to do. And really not much time to do it all.

Everything faced a shadow of doubt, the echoes of failure, the difficulty of life, the lack of control, the pain of loss, the fear of the unknown, the difficulty of unpredictability - I faced them all.

The song of silence - by Simon & Garfunkel. A poignant soft song that echoed the sadness and grief in my heart.

I stared at the abyss of difficulty. I looked upward for answers but I found none. I look sideways to men, yet I found no comfort in those who could not empathize. I found myself increasingly frustrated by human's inability to connect.

Even though life is uncertain, I decidedly know that I must continue my journey. Life is a long stretch, its not easy, its going to hit you like a brick, a tsunami. You will face waves after wave of human disappointments, relationship problems, career issues - yet you can come out stronger after it because you believe that there is something important in life that you still must fulfill.

Life is not just about good results

Nor is it about accumulating greater wealth

Nor is it about gaining power

Nor is it about having all the things you ever wanted

No

It is about finding out your purpose

It is about living a life of purpose

It is about finding what you love

Which really led me to reflect. What would bring me happiness?

I begin to ponder what brought me fulfillment and meaning.

Ray Dalio once said - you can do anything you want, but you cannot do everything you want.

What an important statement.

As 2016 drew to a close, I thought long and hard about what mattered. At the end of life, what really matters?

Perhaps it really boils down to the following 3 questions:

1. Did I find and pursue my calling?

2. Am I a person who kept his promises?

3. Have I left a legacy?

For there is much to do. And really not much time to do it all.

Sunday, August 28, 2016

Is an End-game coming? What should we do?

8 months of 2016 so far

Interestingly, despite 2016 many fearful calls of end-game. The markets appear to be holding up relatively well. The biggest of which appears to be the DJI. It doesn't even discount a Trump Presidency or an interest rate rising environment.

Its amazing what happens in 10 years.

Generally, if you think of life. What "kills" you is not what you saw and know. Its what you didn't see coming. If you crossed the road and didn't see an oncoming car - that could kill you, or injure you.

There are things like buses/lorries that are huge - if they hit you....the damage tends to be more severe. But if you took your necessary precautions, watch the traffic, obeyed the traffic rules....you have a better probability of safety.

Its the same logic with investing. Are the black swans what we see on the horizon?

Absolutely not.

Will Trump presidency cause a recession? I doubt it. But I believe that it will cause some uncertainty in the world where opportunities will arise.

Will a rising interest rate cause a recession? Not entirely, not yet. Maybe when it hits about 3-5%...then you have serious problems. At the current point. No.

So is it possible to see the Black Swans much less predict it? It is hard, but not impossible.

Certain people saw the easy credit and the dangerous practice of asset securitization in the USA. These people like Robert Shiller, John Paulson noticed it. Some raised concerns, some decidedly made billions of dollars from that impending collapse.

The point is the majority failed to see it because it came from a rather secluded part of the banking industry - Asset Backed Securtization.

Here is what I see

1. The big crashes come about every 10 years, think 1987, 1997, 2007 etc.

- Yes. This time it may be different. We never had such an environment before. But do you really want to be on the wrong side of the endgame when it happens?

2. The astronomical debt of countries, QE and negative interest rate

- USA, Japan, ECB. They have continually pushed on with a negative interest rate environment...typically this stimulates the economy and starves off a recession. In the long run, this causes massive inflation and when a collapse really comes. The countries really can only print money...talk about more inflation.

3. Commodity prices have started to pick up, but not as fast as some banks would like it

- The collapse of oil prices and other soft commodities resulted in the banks having an increase in NPL. Companies that are unable to survive this prolong winter will go belly up. The banks have strong balance sheets to handle such a situation. But contagion may happen if the winter holds out too long.

- Low oil prices starves off inflation. Its good for the economy. But low oil prices harm businesses, employment etc....."Damn if you do, damn if you don't".

Then the question comes. Do we sell everything and head for the hills?

The answer is no.

Nobody knows how long all this will happen. Having a good mix of income producing assets. Good value, good businesses will keep the investor steady on his journey to financial independence.

As a rule of thumb

1. Go for investments with yield above 7%

2. Go for companies with relatively lower debt (e.g. <40%)

3. Stick to companies you know (e.g. retail malls you can see, management who are transparent etc.)

Below is a breakdown of analysis of local trusts listed in Singapore. Green is good. Red is not so good. Data extracted from SGX Reit Data (http://reitdata.com/)

Caveat Emptor.

Interestingly, despite 2016 many fearful calls of end-game. The markets appear to be holding up relatively well. The biggest of which appears to be the DJI. It doesn't even discount a Trump Presidency or an interest rate rising environment.

Its amazing what happens in 10 years.

Generally, if you think of life. What "kills" you is not what you saw and know. Its what you didn't see coming. If you crossed the road and didn't see an oncoming car - that could kill you, or injure you.

There are things like buses/lorries that are huge - if they hit you....the damage tends to be more severe. But if you took your necessary precautions, watch the traffic, obeyed the traffic rules....you have a better probability of safety.

Its the same logic with investing. Are the black swans what we see on the horizon?

Absolutely not.

Will Trump presidency cause a recession? I doubt it. But I believe that it will cause some uncertainty in the world where opportunities will arise.

Will a rising interest rate cause a recession? Not entirely, not yet. Maybe when it hits about 3-5%...then you have serious problems. At the current point. No.

So is it possible to see the Black Swans much less predict it? It is hard, but not impossible.

Certain people saw the easy credit and the dangerous practice of asset securitization in the USA. These people like Robert Shiller, John Paulson noticed it. Some raised concerns, some decidedly made billions of dollars from that impending collapse.

The point is the majority failed to see it because it came from a rather secluded part of the banking industry - Asset Backed Securtization.

Here is what I see

1. The big crashes come about every 10 years, think 1987, 1997, 2007 etc.

- Yes. This time it may be different. We never had such an environment before. But do you really want to be on the wrong side of the endgame when it happens?

2. The astronomical debt of countries, QE and negative interest rate

- USA, Japan, ECB. They have continually pushed on with a negative interest rate environment...typically this stimulates the economy and starves off a recession. In the long run, this causes massive inflation and when a collapse really comes. The countries really can only print money...talk about more inflation.

3. Commodity prices have started to pick up, but not as fast as some banks would like it

- The collapse of oil prices and other soft commodities resulted in the banks having an increase in NPL. Companies that are unable to survive this prolong winter will go belly up. The banks have strong balance sheets to handle such a situation. But contagion may happen if the winter holds out too long.

- Low oil prices starves off inflation. Its good for the economy. But low oil prices harm businesses, employment etc....."Damn if you do, damn if you don't".

Then the question comes. Do we sell everything and head for the hills?

The answer is no.

Nobody knows how long all this will happen. Having a good mix of income producing assets. Good value, good businesses will keep the investor steady on his journey to financial independence.

As a rule of thumb

1. Go for investments with yield above 7%

2. Go for companies with relatively lower debt (e.g. <40%)

3. Stick to companies you know (e.g. retail malls you can see, management who are transparent etc.)

Below is a breakdown of analysis of local trusts listed in Singapore. Green is good. Red is not so good. Data extracted from SGX Reit Data (http://reitdata.com/)

Caveat Emptor.

Sunday, August 14, 2016

Passing the final exam of the CFA, Joseph Schooling and finding a purpose in life

On August 09, the day the country celebrated national day. I received my CFA Level 3 results about 9.30pm. The congratulatory tone was a happy sound within my world - it brighten my family world for just a bit.

If any case, I would take no credit for this. No one reaches the pinnacle of success on his own.

For that, I would like to dedicate this to my father, my mother, my siblings, my friends and my colleagues that constantly edged me forward towards chasing my dreams. None of this would have been possible without encouragement during the particularly difficult year.

Now I seek a new job, to gather the experiences that would allow me to make my mark in the investment industry. I am excited about the area of impact investing and truly believe that the world can be a better place if we put our heart to making it so.

The country's first world champion

On Aug 13th, the nation of Singapore won its first ever gold medal through a young boy called Joseph Schooling. What people see as a 50.39sec - 100m butterfly swim is actually years and countless hours of training, of family effort, of parental love, of long early hours in the pool, of difficult times navigating NS deferment, much investment by his own family and the difficulty staying away from your home country.

What Joseph Schooling proved is that - little countries can do amazing things. All you need to do is to put your heart to it and keep going forward. It is amazing, and he thoroughly won my respect. A true inspiration.

Purpose in life

Many people go through life just plugging through the motions. Wasting time playing games, spending it on people who don't matter, chasing hobbies that do not add value to society. I began to realize this year that is not the life I want. I don't want to live a boring life that just does what an employer asks you to do, being a follower and not a leader, and ultimately not making people life better.

After reading the inspirational book "How will you measure your life" by the Harvard professor Clayton M. Christensen. I begun to ponder what is it that I want for this life. We have all but one life to live - how will we live it?

As he said "Figuring out the purpose of your life is the singular most important thing in life"

After thinking it through, I came up with 3 points:

1. To be a role model in society - someone that my parents, my family, my (future) spouse and my friends will be proud of.

2. To practice kindness, uphold integrity and stay true to striving for high standards in all things

3. To improve the lives of people around me, to help deal with their problems and to ultimately start a foundation that helps the sick and needy. That is to become someone that is deeply spiritual and cares for his fellow people.

Saturday, August 13, 2016

DBS and the unfortunate case of swiber

http://www.straitstimes.com/business/banking/dbs-chief-fails-to-ease-analyst-discomfort-over-oil-and-gas-exposure

Reading the above article raises some room for concern to DBS as a long term investment.

1. The management extended the loan on the basis of an investor (AMTC) that has dragged his feet in investing in the company - if the private equity is having concerns with the investment in the company, I think the bankers should be even more conservative, not aggressive.

2. To prop up your local champions is admirable. But Singapore has always had the history of letting things that are not viable, fail - think Stats Chipac, NOL, etc. What makes DBS so special to help this company to the extent?

3. The management were caught off guard. This is the most shocking. CEO Piyush is constantly seen as the man with the big picture and detail oriented mindset. I am slightly astounded by the fact that he could be caught off guard. Worse still, the swiber management team did not even keep DBS as the principal banker in the loop - causing much shock and awe and losses of about 3.6bln to DBS market cap.

What is credit analysis all about?

This is a classic case of character consideration. In credit analysis, the 3 Cs that are most critical are

1. Character

2. Collateral

3. Capitalization

Given that number 3 was a big problem - i.e. no equity based left, its a very big concern why DBS should increase its loans from an estimated 100m to 700m.

Collateral, such distressed assets have minimal collateral....but providing working capital for a lightly capitalized company basically means you are investing in a company with very high risk....

Character, sadly it seems that the character assessment by the RMs failed when the board and management team of swiber decided to liquidate without consulting their bankers.

What happens now?

Quite likely, DBS will escape relatively unscathed given the large amount of assets. However, it brings concerns to the risk management ability which it says there would be 'no change'. Either its a show of marketing to the public or that the management is heading down the road to a very deadly end.

What is most important is not to ask what DBS can get back but the contagion that may breakout as a result of one company going bust (suppliers may stop providing supplies, clients may stop paying, banking loans may freeze up, banks may earmark and block your loans etc.).

Would this happen to other oil industry companies because of one player? - quite possibly. And then you may see the big hit to DBS's balance sheet - contagion if it happens will be something that would reverse all the good work that wealth management has done so far for the company.

IF anything positive, it would be that the company is very open telling you their exposures. Which is significant (as per below)

Investors beware - Caveat Emptor.

Bloomberg has sound the warning bells - https://www.bloomberg.com/gadfly/articles/2016-08-08/dbs-soured-loans-mask-something-more-disturbing

Reading the above article raises some room for concern to DBS as a long term investment.

1. The management extended the loan on the basis of an investor (AMTC) that has dragged his feet in investing in the company - if the private equity is having concerns with the investment in the company, I think the bankers should be even more conservative, not aggressive.

2. To prop up your local champions is admirable. But Singapore has always had the history of letting things that are not viable, fail - think Stats Chipac, NOL, etc. What makes DBS so special to help this company to the extent?

3. The management were caught off guard. This is the most shocking. CEO Piyush is constantly seen as the man with the big picture and detail oriented mindset. I am slightly astounded by the fact that he could be caught off guard. Worse still, the swiber management team did not even keep DBS as the principal banker in the loop - causing much shock and awe and losses of about 3.6bln to DBS market cap.

What is credit analysis all about?

This is a classic case of character consideration. In credit analysis, the 3 Cs that are most critical are

1. Character

2. Collateral

3. Capitalization

Given that number 3 was a big problem - i.e. no equity based left, its a very big concern why DBS should increase its loans from an estimated 100m to 700m.

Collateral, such distressed assets have minimal collateral....but providing working capital for a lightly capitalized company basically means you are investing in a company with very high risk....

Character, sadly it seems that the character assessment by the RMs failed when the board and management team of swiber decided to liquidate without consulting their bankers.

What happens now?

Quite likely, DBS will escape relatively unscathed given the large amount of assets. However, it brings concerns to the risk management ability which it says there would be 'no change'. Either its a show of marketing to the public or that the management is heading down the road to a very deadly end.

What is most important is not to ask what DBS can get back but the contagion that may breakout as a result of one company going bust (suppliers may stop providing supplies, clients may stop paying, banking loans may freeze up, banks may earmark and block your loans etc.).

Would this happen to other oil industry companies because of one player? - quite possibly. And then you may see the big hit to DBS's balance sheet - contagion if it happens will be something that would reverse all the good work that wealth management has done so far for the company.

IF anything positive, it would be that the company is very open telling you their exposures. Which is significant (as per below)

Investors beware - Caveat Emptor.

Bloomberg has sound the warning bells - https://www.bloomberg.com/gadfly/articles/2016-08-08/dbs-soured-loans-mask-something-more-disturbing

Knowing what you don't know and Keppel T&T

Sometimes people ask me for tips on things to buy, what to invest, how do I invest, how do I know so much etc.

Honestly, there isn't a lot of secrets. It all boils down to the effort you put in to set up the trade on the investment. Some people spend so much time saving on the few cents, making sure they get the best prices on food, vegetables, housing. But they spend so little time on their investments (Which are not small at all)

Take for example, a recent case of a market run up with keppel T&T. The purchase we made was at 1.41 and it had a good run up to 1.74 before falling back to 1.6 range.

Am I selling? No.

Am I buying? Perhaps.

Why, you may ask...

The appraisal of the investment community of the better prospects of data centre fund investing has yet to materialize. Also, I bought the shares on the basis of several catalysts which I have not seen appear

The catalyst(s) are

1. Sale of the data centre to keppel DC reit

2. IPO of logisitics reit in Indonesia (growth market)

3. Privatization of Kep T&T

4. Sale of M1 stake and distribution of cash

The margin of safety:

1. Rise in prices of keppel DC reit and M1 (keeps improving)

Honestly, there isn't a lot of secrets. It all boils down to the effort you put in to set up the trade on the investment. Some people spend so much time saving on the few cents, making sure they get the best prices on food, vegetables, housing. But they spend so little time on their investments (Which are not small at all)

Take for example, a recent case of a market run up with keppel T&T. The purchase we made was at 1.41 and it had a good run up to 1.74 before falling back to 1.6 range.

Am I selling? No.

Am I buying? Perhaps.

Why, you may ask...

The appraisal of the investment community of the better prospects of data centre fund investing has yet to materialize. Also, I bought the shares on the basis of several catalysts which I have not seen appear

The catalyst(s) are

1. Sale of the data centre to keppel DC reit

2. IPO of logisitics reit in Indonesia (growth market)

3. Privatization of Kep T&T

4. Sale of M1 stake and distribution of cash

The margin of safety:

1. Rise in prices of keppel DC reit and M1 (keeps improving)

2. Data centre business performing very strongly

3. Logistics poorly performing but asset value retains

What about the impending crash and brexit and Donald Trump?

There was a saying. In life there are knowledge - you know what you know. And areas that are lacking - what you don't know. If you know what you know, and you know what you don't know - you know everything. Ray Dalio is a fantastic proponent of his logic and he acts to find people to cover the knowledge gap.

Read the Ray Dalio article below:

http://www.forbes.com/sites/kerryadolan/2016/05/02/billionaire-hedge-fund-manager-ray-dalio-on-why-hes-a-professional-mistake-maker/#77e7333d53e3

Saturday, June 11, 2016

Musings about Investment Themes - eCommerce (Global Logistics Properties - MC0.SI)

As I was pondering over the markets recently. We start to see very quality assets that are starting to emerge.

Investment Themes that will do very well over the next few years are

1. Big Data (and its storage)

2. eCommerce (and its storage)

3. Frontier Markets (Myanmar)

4. Clean Energy (and its various components)

5. Urbanization of cities

Pointing to Theme 2 in particular - eCommerce

One particular company that caught my eye is Global Logistics Properties (GLP). GLP is a market leader in China with a large footprint worldwide in USA/ Japan/Brazil. Interestingly, GLP was a company born from the global financial crisis in 2008. It succeeded with the a management buyout of prologis assets with the backing of GIC.

Fast forward 8 years. The company was listed, and continue to flourish as a builder, asset manager and operator with high occupancy of its high tech logistics (glorified warehouse).

3 questions always come to mind when investing.

1. Does the company have a strong investment theme?

Yes. Being right in the heart of china where eCommerce is booming (think Baidu/Alibaba/JD.com/Tencent) - there is much opportunity to support all these companies who require the logistics know how as they advance towards selling their products

2. Does GLP have a moat?

Yes. The network effect has been much touted by the company itself. The network effect is the strength of a company that grows as its community grows larger. In this case, the network effect is relevant for the customer if he wants to say sell his product in different parts of China. GLP can help to provide a different cost package or an assistance to move the goods accordingly to different places.

3. Is the company highly leveraged?

To the contrary. No. Debt gearing is about 30%. Which is pretty reasonable and gives ample gunpowder should opportunity arises. The company also exercise prudence in terms of development - they cut back on capex from 1.7bln to 1.4bln (warehouse developments) as they are seeing logistic occupancy fall below 90%. Should it rises above 90% again (i.e. economy picks up). They will increase capex once more.

What is the worse that could happen?

China debt bubble implodes, causing a freeze up of capital flow, consumer shock, massive cutback on spending and job cuts - Financial Armageddon. Share price may fall to about 1.20.

Likely hood: Pretty low, but some adjustments within china are currently in place to mitigate this issue.

1.20 price is an even better price to buy a wonderful company.

Target price: 2.47

(Provided by DBS Vickers - https://www.dbs.com.sg/treasures/aics/EquityArticle.page?dcrPath=templatedata/article/equity/data/en/DBSV/012014/GLP_SP.xml)

(The author is vested with 3300 shares as of the time of writing)

Investment Themes that will do very well over the next few years are

1. Big Data (and its storage)

2. eCommerce (and its storage)

3. Frontier Markets (Myanmar)

4. Clean Energy (and its various components)

5. Urbanization of cities

Pointing to Theme 2 in particular - eCommerce

One particular company that caught my eye is Global Logistics Properties (GLP). GLP is a market leader in China with a large footprint worldwide in USA/ Japan/Brazil. Interestingly, GLP was a company born from the global financial crisis in 2008. It succeeded with the a management buyout of prologis assets with the backing of GIC.

Fast forward 8 years. The company was listed, and continue to flourish as a builder, asset manager and operator with high occupancy of its high tech logistics (glorified warehouse).

3 questions always come to mind when investing.

1. Does the company have a strong investment theme?

Yes. Being right in the heart of china where eCommerce is booming (think Baidu/Alibaba/JD.com/Tencent) - there is much opportunity to support all these companies who require the logistics know how as they advance towards selling their products

2. Does GLP have a moat?

Yes. The network effect has been much touted by the company itself. The network effect is the strength of a company that grows as its community grows larger. In this case, the network effect is relevant for the customer if he wants to say sell his product in different parts of China. GLP can help to provide a different cost package or an assistance to move the goods accordingly to different places.

3. Is the company highly leveraged?

To the contrary. No. Debt gearing is about 30%. Which is pretty reasonable and gives ample gunpowder should opportunity arises. The company also exercise prudence in terms of development - they cut back on capex from 1.7bln to 1.4bln (warehouse developments) as they are seeing logistic occupancy fall below 90%. Should it rises above 90% again (i.e. economy picks up). They will increase capex once more.

What is the worse that could happen?

China debt bubble implodes, causing a freeze up of capital flow, consumer shock, massive cutback on spending and job cuts - Financial Armageddon. Share price may fall to about 1.20.

Likely hood: Pretty low, but some adjustments within china are currently in place to mitigate this issue.

1.20 price is an even better price to buy a wonderful company.

Target price: 2.47

(Provided by DBS Vickers - https://www.dbs.com.sg/treasures/aics/EquityArticle.page?dcrPath=templatedata/article/equity/data/en/DBSV/012014/GLP_SP.xml)

(The author is vested with 3300 shares as of the time of writing)

Saturday, April 30, 2016

Update on Ascendas H Trust

Reflections.

Ascendas H Trust plunged some 13% in one day post management announcement that it is ending all talks with takeover interests.

There I was sitting on a significant loss account. Basically you have 3 options when you are purchasing a stake.

1. You keep your entire stake

2. You sell your entire stake

3. You sell part of your stake

When I entered this trade, it was solely on the basis of a takeover offer. Which when it failed to materialize, a trader would decide to get out asap. So this likely accounted for the sharp plunge.

As I entered as a trader, I was quite ready to get out.

But then, to take a large loss is not easy. What should you do then?

You evaluate the scenarios and the assumptions you went through earlier. This is to avoid bounded rationality where one does not seek full information but make do with the most recent or available information making sub-optimal decisions.

I evaluated my choices and went with choice 3.

I sold down a small portion, and kept about 80% of the stake. I evaluated this on a total portfolio basis as well as I sold down my capitacommercial trust stake concurrently.

This is the following reasons:

1. This is a yield accretive move. 7.6% on my purchase price vs 6% from capitacommercial

2. Office reits are in a precarious position as a large supply of Grade A office are coming in

3. The recovery story of Ascendas H trust is very much intact, AUD is rising, australia economy has a certain attraction and strength

4. Management's commitment to enhancing returns to shareholders - saying no is just as important as saying yes. If an offer undervalues the asset, the management should act in the best interest of their shareholders and keep the faith.

Why then did I sell down 20%?

This is to manage the overall portfolio, certainly there are better opportunities down the road. Think when the Fed raise interest rates again or if china devalues the yuan or if the bad debt of china implodes or if Britain suddenly goes Brexit.

Anyone of the above 4 factors can cause a 20% plunge in blue chips. The volatility is very excellent for traders. But even for long term investors, one should rejoice in the sight of a sale.

Did I make a mistake?

I did my valuations the consideration that the PE and acquirers were all conducting their valuations independent of the valuator's final calculation. This is definitely something to learn from.

As long term investors - Its all about consistency, longevity and a sound process of execution. Rinse and repeat.

After all, "Not everything that counts can be counted, and not everything that can be counted counts."

- Albert Einstein

Ascendas H Trust plunged some 13% in one day post management announcement that it is ending all talks with takeover interests.

There I was sitting on a significant loss account. Basically you have 3 options when you are purchasing a stake.

1. You keep your entire stake

2. You sell your entire stake

3. You sell part of your stake

When I entered this trade, it was solely on the basis of a takeover offer. Which when it failed to materialize, a trader would decide to get out asap. So this likely accounted for the sharp plunge.

As I entered as a trader, I was quite ready to get out.

But then, to take a large loss is not easy. What should you do then?

You evaluate the scenarios and the assumptions you went through earlier. This is to avoid bounded rationality where one does not seek full information but make do with the most recent or available information making sub-optimal decisions.

I evaluated my choices and went with choice 3.

This is the following reasons:

1. This is a yield accretive move. 7.6% on my purchase price vs 6% from capitacommercial

2. Office reits are in a precarious position as a large supply of Grade A office are coming in

3. The recovery story of Ascendas H trust is very much intact, AUD is rising, australia economy has a certain attraction and strength

4. Management's commitment to enhancing returns to shareholders - saying no is just as important as saying yes. If an offer undervalues the asset, the management should act in the best interest of their shareholders and keep the faith.

Why then did I sell down 20%?

This is to manage the overall portfolio, certainly there are better opportunities down the road. Think when the Fed raise interest rates again or if china devalues the yuan or if the bad debt of china implodes or if Britain suddenly goes Brexit.

Anyone of the above 4 factors can cause a 20% plunge in blue chips. The volatility is very excellent for traders. But even for long term investors, one should rejoice in the sight of a sale.

Did I make a mistake?

I did my valuations the consideration that the PE and acquirers were all conducting their valuations independent of the valuator's final calculation. This is definitely something to learn from.

As long term investors - Its all about consistency, longevity and a sound process of execution. Rinse and repeat.

After all, "Not everything that counts can be counted, and not everything that can be counted counts."

- Albert Einstein

Thursday, March 31, 2016

Special Situation - M&A - Ascendas Hospitality Trust

BUY Call (Deep value with 25% upside over an 8 month horizon)

By Joel

Current Price: $0.75

Target price: $0.93

Upside value 24.6%

|

| Relative valuation of Ascendas H Trust (data obtained from SGX Reit Data - ReitData.com) |

Value = [Graham ratio (20%) + DBS valuation (15%) + NAV (50%) + Worse case scenario (15%)]x 1.10 (buyout premium)

Background:

I have observed Ascendas H Trust since its announcement on 23rd December 2015 that it received an unsolicted offer to buyout the reit position. This perk my interest and I began tracking this stock.

The lack of movement above $0.75 range appears to show that one of the offer was probably in that range. I expect additional offer(s) to come in as there appears to be a possible bidding war (helps to be the buyout target - think of F&N buyout in 2012-2013).

Management brought forward independent valuation of properties to evaluate offers - emphasis on the plural form.

Assumption

1. 10% buyout premium is used

2. Upward revaluation of assets to $0.842 (from $0.72) shows significant value and consideration of tabled offer by management (strategic review) will be completed soon

3. Comparison was used with gearing, yield and book value

Background:

I have observed Ascendas H Trust since its announcement on 23rd December 2015 that it received an unsolicted offer to buyout the reit position. This perk my interest and I began tracking this stock.

The lack of movement above $0.75 range appears to show that one of the offer was probably in that range. I expect additional offer(s) to come in as there appears to be a possible bidding war (helps to be the buyout target - think of F&N buyout in 2012-2013).

Reasons I am buying Ascendas H Trust

1. Several buyers have tabled offers (Starwood Capital / Fosun / Gaw Capital / Blackstone)

2. Upside of 25% is 3 times downside of 8%

3. Defensive nature of reit structure being 90% dividend payout and 7.73% trailing yield + Australia tourism continues to pick up

Risks

1. Substantial shareholder - Tong Jinquan sells out at 0.765

2. Australia RevPAR fell 5% year on year (crown jewel)

3. High gearing at 38.2% / All in interest rate 3.4% / 2.3 years to maturity

Addressing risk concerns

- Gearing is lowered given the upward revaluation - gearing should be reduced to around 33%

- Nature of Australian financing loans tend to be higher (interest rate is high in the country)

- Improving tourism and the relatively weaker AUD should help push up RevPAR over time

- Ascendas looking to do refinancing of 2016 loans

Only risk that I cannot pinpoint is the reason why Tong Jinquan sold out. It is possible that he holds the asset for income yielding asset tool, given the privatization nature, he doesn't need it anymore.

As of 31/03/16. The author owns shares in the above mentioned company.

Sunday, January 17, 2016

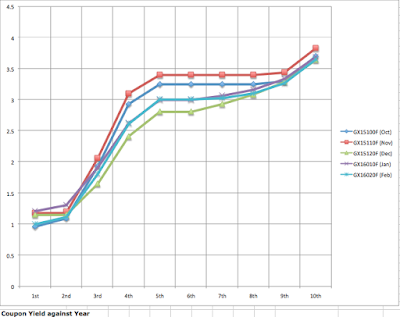

Economic Armageddon? Where to allocate your assets now (Part 2/4) - SSB and Reits

SSB

I was analyzing the Singapore Savings Bonds - 5 issues to date.

Here were some interesting points

1. November continue to dominates all the bond issues

2. The demand is tepid but could likely be around 40m monthly

3. Some High Net worth individuals are trying to park more money than permitted (approximately 2+ million of oversubscription without getting allocated)

My takeaway:

1. It appears that fear is entering the market, 10 year bond prices are going up therefore pushing the yield curve down comparing Dec - Feb issue vs Oct and Nov

2. In the short term, interest rate is expected to hike so subsequent issues should be better

3. The rich are beginning to fear the markets, asset allocation to safer assets may be prudent for all investors now (smart money moves)

Appended is the comparison for your use.

I was analyzing the Singapore Savings Bonds - 5 issues to date.

Here were some interesting points

1. November continue to dominates all the bond issues

2. The demand is tepid but could likely be around 40m monthly

3. Some High Net worth individuals are trying to park more money than permitted (approximately 2+ million of oversubscription without getting allocated)

My takeaway:

1. It appears that fear is entering the market, 10 year bond prices are going up therefore pushing the yield curve down comparing Dec - Feb issue vs Oct and Nov

2. In the short term, interest rate is expected to hike so subsequent issues should be better

3. The rich are beginning to fear the markets, asset allocation to safer assets may be prudent for all investors now (smart money moves)

Appended is the comparison for your use.

Real Estate Investment Trust (REIT) and other Trusts

A REIT is a beautiful way to grow your assets and your nest egg. Now I don't advocate you to plonk your entire house (bet the house) in it, but it definitely plays a very important role in times like this.

Here are some interesting facts about REITS:

1. They have to distribute 90% of net income to unit holders

2. They are managed assets with built in inflationary contracts (i.e. revision to rental rates)

3. They can give good yield and are rather defensive in nature (i.e. will not fall much in times of recession)

The following was collated from SG Reits. A fantastic site for getting the latest data. After some data crunching. High Yield assets >7% and Debt Gearing <35% (Total Debt/ Total Assets). I came up with the following 10 cases.

Each has some compelling case and will likely be rewarding to the long term investor.

This is not an advise to invest blindly, but certainly a decent allocation to REIT will help in asset growth.

Caveat emptor. Please carry out individual in-depth analysis on each case.

Economic Armageddon? Where to allocate your assets now (Part 1/4)

Judging from the first two weeks of market movements. Some recurring themes appear more apparent now:

1. Oil prices is not coming back. Not for a while. Expect oil and offshore marine to be badly affected, possibly not coming back till 2018. If you are a long term investor it may pay to hold assets there in a cyclical run - but there is plenty of time to get back in on this trend. Oil is expected to go down to USD20 and maybe even USD10.

2. The interest rate hike in USA appears to have open up a can of worms. How can the Fed hike the rates when the economy does not look like it is on the growth path. Perhaps the rate hike has come a little too late. But that being said, slow hike will allow for gradual adjustments by companies. The debt binge has been a constraint on the US economy. Printing of money will not do when USD is no longer the major reserve. China is putting the CNH/CNY quite firmly on the map with the establishment of the AIIB (Asian Infrastructure Investment Bank) and addition to the Special Drawing Rights (SDR). It will join the euro, yen, pound and dollar in the reserves basket. The yuan will have about an 11 percent weighting in the SDR. This places China in a strong position to become the next superpower.

3. In terms of attractiveness. Europe and USA appears quite attractive in terms of the quality of domestic consumption (or so the economists believe). One thing is for sure, hot capital is flowing out of Asia quite rapidly in the purported 'flight to safety', the flow back to the developed nations should give those countries some needed boost to their economy.

4. Europe remains a periphery of immigrant issues. The quack-mire mix of massive immigrants / distrust / lack of employment / politics and terrorism will continue to be the biggest risk for those countries

5. For USA, the future looks the brightest with capitalism leading the way. Having either president Trump or Hilary should not have a major impact on the direction of the country (being I believe they are both capable individuals quite befitting of the roles)

6. The biggest risk for Asia remains the mountain of debt among Chinese companies. In addition, given that Asia has huge exposure to the chinese economy in terms of consumption, commodities and manufacturing. It is quite clear that NPL (Non Performing loans) of banks and defaults will occur more rapidly. The clock has turned for Asia and we are already in a recession.

Putting it altogether. Where is a good place to put your money?

Depending on your risk profile, I believe some blue chips value are starting to emerge, I have also begin to see companies that are potential multi-baggers, I will write about these cases on another article.

Part 2 - Discussion on safer/safest assets - Singapore Saving Bonds / Bank Deposits / REITS

Part 3 - Blue Chips

Part 4 - Multibaggers

1. Oil prices is not coming back. Not for a while. Expect oil and offshore marine to be badly affected, possibly not coming back till 2018. If you are a long term investor it may pay to hold assets there in a cyclical run - but there is plenty of time to get back in on this trend. Oil is expected to go down to USD20 and maybe even USD10.

2. The interest rate hike in USA appears to have open up a can of worms. How can the Fed hike the rates when the economy does not look like it is on the growth path. Perhaps the rate hike has come a little too late. But that being said, slow hike will allow for gradual adjustments by companies. The debt binge has been a constraint on the US economy. Printing of money will not do when USD is no longer the major reserve. China is putting the CNH/CNY quite firmly on the map with the establishment of the AIIB (Asian Infrastructure Investment Bank) and addition to the Special Drawing Rights (SDR). It will join the euro, yen, pound and dollar in the reserves basket. The yuan will have about an 11 percent weighting in the SDR. This places China in a strong position to become the next superpower.

3. In terms of attractiveness. Europe and USA appears quite attractive in terms of the quality of domestic consumption (or so the economists believe). One thing is for sure, hot capital is flowing out of Asia quite rapidly in the purported 'flight to safety', the flow back to the developed nations should give those countries some needed boost to their economy.

4. Europe remains a periphery of immigrant issues. The quack-mire mix of massive immigrants / distrust / lack of employment / politics and terrorism will continue to be the biggest risk for those countries

5. For USA, the future looks the brightest with capitalism leading the way. Having either president Trump or Hilary should not have a major impact on the direction of the country (being I believe they are both capable individuals quite befitting of the roles)

6. The biggest risk for Asia remains the mountain of debt among Chinese companies. In addition, given that Asia has huge exposure to the chinese economy in terms of consumption, commodities and manufacturing. It is quite clear that NPL (Non Performing loans) of banks and defaults will occur more rapidly. The clock has turned for Asia and we are already in a recession.

Putting it altogether. Where is a good place to put your money?

Part 2 - Discussion on safer/safest assets - Singapore Saving Bonds / Bank Deposits / REITS

Part 3 - Blue Chips

Part 4 - Multibaggers

Subscribe to:

Posts (Atom)