Today's topic is about Special Situation investing.

For the uninitiated, Special Situations refer to any of the below scenarios:

1. Merger & Acquisition

2. Asset Sales & Purchase

3. Recapitalization and turnaround

etc.

If you know what you are doing. Sometimes a very complicated deal may make sense. But if you don't know what you are doing, there is no shame in admitting it. Only when people pretend they are experts, then its a real shame - plonking money in something you don't understand is really gambling.

Personally in the field of special situations - I admit, I have much to learn and have bought Joel Greenblatt book "You can be a stock market genius" - apparently the best selling primer on such deals which I come to love and appreciate.

Now on to the case:

Recently I did a simple analysis for

RHT Healthtrust. A quick introduction as below:

RHT healthtrust owns healthcare assets in India. Leasing the asset to its parent company Fortis. As of 14th Nov, Fortis decided they have a change of heart (strategy) and wanted to go asset heavy once more.

This news caused the share price to surge 15% on the news. People were a little murky on the details and couldn't figure out the price with debt, without debt repayment etc.

I had half a mind to jump in immediately, but some quiet meditation and thoughtful thinking later, I decided to let the dust settle first before looking at the deal.

As of couple of days back, the price fell within a sweet spot. Which I call the low risk high return quantum of minimum 3x upside compared to the downside.

How did I derive upside price? Here's my 3 part analysis

Part 1: Figuring out what the deal is worth

Given that the deal is valued about 46.5 bln rupees. And paying off the debt, the offer values the company around the range of 765m SGD. This would give an offer price about $0.94. Adding some accrued dividends, we should get a final price of $0.97. The deal takes a big chunk and matters most, therefore a 50% weight is a minimum.

Part 2: Taking into account what the analysts think

Taking a simple average of 4 analysts - we get an average of $0.8875. Given they are experts, I give them a 30% weight.

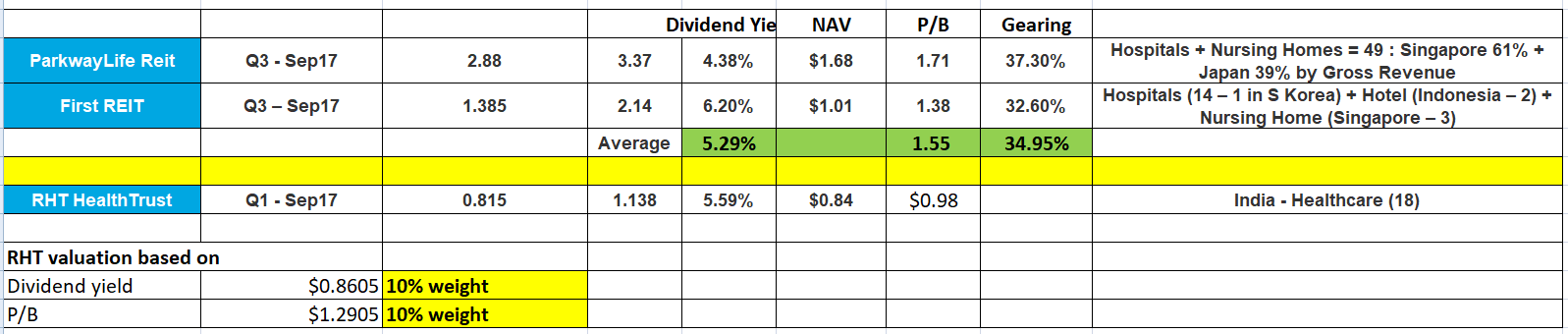

Part 3: Some basic due diligence (Relative Valuation)

Using the only peers available on the SGX, Parkway life and First Reit. You get two very different players but in similar business of leasing out healthcare assets. Using dividend yield, P/B we come up with two values.

Dividend Yield gives about $0.8605. P/B gives a value of $1.2905. By the PB ratio basis, this deal is really undervaluing the potential of the company, dividend wise - about the normal.

I gave both valuations 10% weight each.

Assumptions:

1. FX (INR-SGD) remains constant

2. Company does a payout of cash and dividend

3. Deal goes through with no competing buyers (this is actually positive on the upside but affects the deal timeline)

4. Company pays down debt, pays out cash and winds up the business

Downside

Quantitative risk

1. Blockage/Deal does not go through - company worth intrinsic value of 0.84

2. Lowest closing price of 0.795 and lowest 52 week price 0.71

Price Average 0.782

Downside risk -4.09%

Qualitative risks

1. Depreciation of INR

2. Other possible risk such as Fortis going belly up/unable to raise capital are minimal given standard chartered's commitment to a 50bln rupees capital raising event

3. Parent has yet to pay relevant fees for half year (potential query as to its cashflow issue)

Announcement 15-Nov

Time frame 60 days

Expected conclusion 14-Jan

Remaining days 33 (as of 15 Dec)

Weighted price expectation $0.971

Purchase Price 15-Dec @ 0.82

Expected returns 18.42%

Annualized return 203.76%

Final conclusion: Buy by sizing (no more than 10% of portfolio due to country risk) 4.5x upside vs downside.

Disclosure: Author has a small sizable position of 5% of his portfolio in the deal.